2018 has been an interesting year. Ok, that is the polite way of saying it’s the kind of year that is a bit frustrating. At the beginning of the year, I talked about inflation and rising interest rates being the biggest headwinds that the markets would need to digest. By late February and early March, the current administration started to add tariffs and has continued to escalate both the rhetoric and the actions against foreign economies. That brings us to the month of October…

Let me start by saying that very little has changed in the overall economy from September to October. Often times when volatility picks up, investors are concerned that a recession is imminent. Most analysts do not see that on the horizon this year and short of a major policy misstep by the Federal Reserve, I think it is unlikely to happen soon. Unemployment is low, wages are starting to increase, inflation is in the Fed’s “Goldilocks Zone” at 2%, and business and consumer confidence remains high. There are headwinds, to be sure, but every single one of those headwinds have been in place all year long. Trade policy, rising interest rates, and perhaps more importantly, a lack of interest in the fundamentals of company earnings are a few examples.

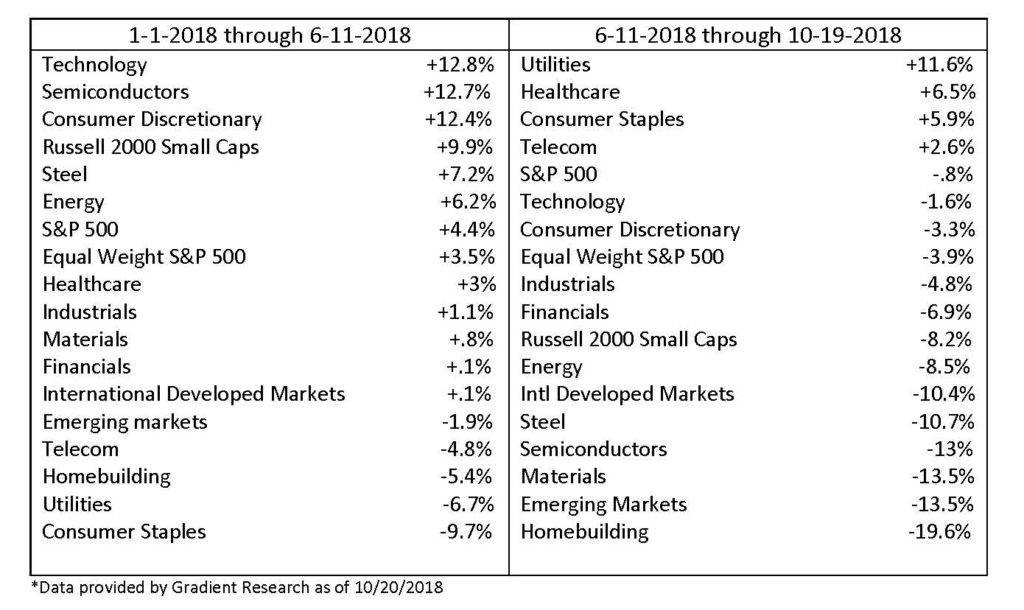

This last item is what I would like to focus on today. Most of the S&P’s performance this year, so far, has been driven by a handful of companies – some of you have heard the acronym FAANG. Looking at the Tech sector vs. the broader sector indexes we see the disparity between them and the performance of those broader indexes on the S&P 500.

The expectations for some of these companies and sectors could have been too high. If the economy is doing well, and by most expectations we should be somewhere around 3% to 3.5% GDP this year, then it seems that two things are happening.

1) There is an expectation that Trade Policy will hurt or is currently hurting sectors like Industrials, Materials, and Steel. That certainly was born out this week by global Fortune 500 Industrial companies earnings reports. Auto manufacturers have struggled all year as have many companies that need raw materials as part of the manufacturing process. Input costs have risen for many of these companies between the first and third quarters as a result of tariffs. In many cases, the fundamentals of companies in these sectors look good or even great but geopolitical risks are holding them back.

2) Sectors that are sensitive to rising interest rates have split in two directions. Homebuilders have been disproportionately affected by a .75% rise in interest rates from a year ago. Energy stocks have been sold off on concerns of rising interest rates on high debt levels. Telecom and Utilities, normally sectors that act inversely to interest rates, have climbed. Rotation into areas of the economy that will be less affected by tariffs makes sense and by and large, I think that is what we are seeing over the last few months. However, we are seeing the same short term phenomenon – well run and profitable companies are being ignored based on concerns about the future of interest rates.

I use these examples to illustrate that 2018 is, indeed, a year that has forgotten the fundamentals of investing. At Blue Dot Wealth Management, we look for companies across all sectors that have a combination of low debt, strong earnings growth, below sector average Price to Earnings ratios, and strong ESG ratings. Over time, companies that grow responsibly and are trading at a value tend to outperform their peers. This Growth at a Reasonable Price philosophy works over time but when markets are faced with geopolitical or policy uncertainty, similar to the kinds we saw in 2011, 2013, and to a smaller extent 2016, the fundamentals of individual companies are often times ignored. While we can’t control trade policy or interest rates (or elections or the debt ceiling, etc), we can control the kinds of companies we invest in. Good old fashioned fundamentals matter over time. This particular storm will pass at some point and when it does, I am confident we will see a focus on valuations and earnings growth.

These are the opinions of Robert Young and not necessarily those of Cambridge, are for informational purposes only, and should not be construed or acted upon as individualized investment advice. Diversification and asset allocation strategies do not assure profit or protect against loss. Indices mentioned are unmanaged and cannot be invested into directly. Past performance is no guarantee of future results. Investing involves risk. Depending on the types of investments, there may be varying degrees of risk. Investors should be prepared to bear loss, including total loss of principal.